Sustainability reporting will be mandatory from 2024 - and will affect both large and small companies!

The CSRD (or "Corporate Sustainability Reporting Directive") is an EU directive that requires companies with more than 500 employees to report on their sustainability profile. The directive will be incorporated into Danish legislation from 1 July 2024.

Initially, the requirements of the CSRD directive affect companies in accounting class D with 500+ employees. However, smaller companies are indirectly affected by the requirements placed on the larger companies, where i.a. "CO2 emissions in the supply chain" will be a measurement point.

Regardless of whether you are a large or small company, you will most likely need to be able to work structured with data when the CSRD directive enters into force in 2024.

What is CSRD?

CSRD stands for "Corporate Sustainability Reporting Directive", and is an EU directive that requires companies to report on their work with sustainability.

In short, the CSRD directive from the EU requires companies with more than 500 employees to integrate sustainability reporting as part of their current management report.

That something is a \"directive\" means that the directive's guidelines must be implemented and enforced through national law. In Denmark, we can expect the first proposal for this to be adopted and implemented from July 1, 2024 (correction to the Danish Financial Statements Act, May 22, 2024).

Why is the CSRD Directive significant?

In 2024, the content of the CSRD directive will be enforced through legislation - and thus a matter of compliance.

For large companies with more than 500 employees, the CSRD directive initially means that you have to deal with ESG data and sustainability reporting to a completely different extent than what you have previously been used to.

For smaller companies that are not covered by the rule of 500 employees, you can gradually start preparing for larger companies in the value chain to require that data can be provided about products and services traded across the companies.

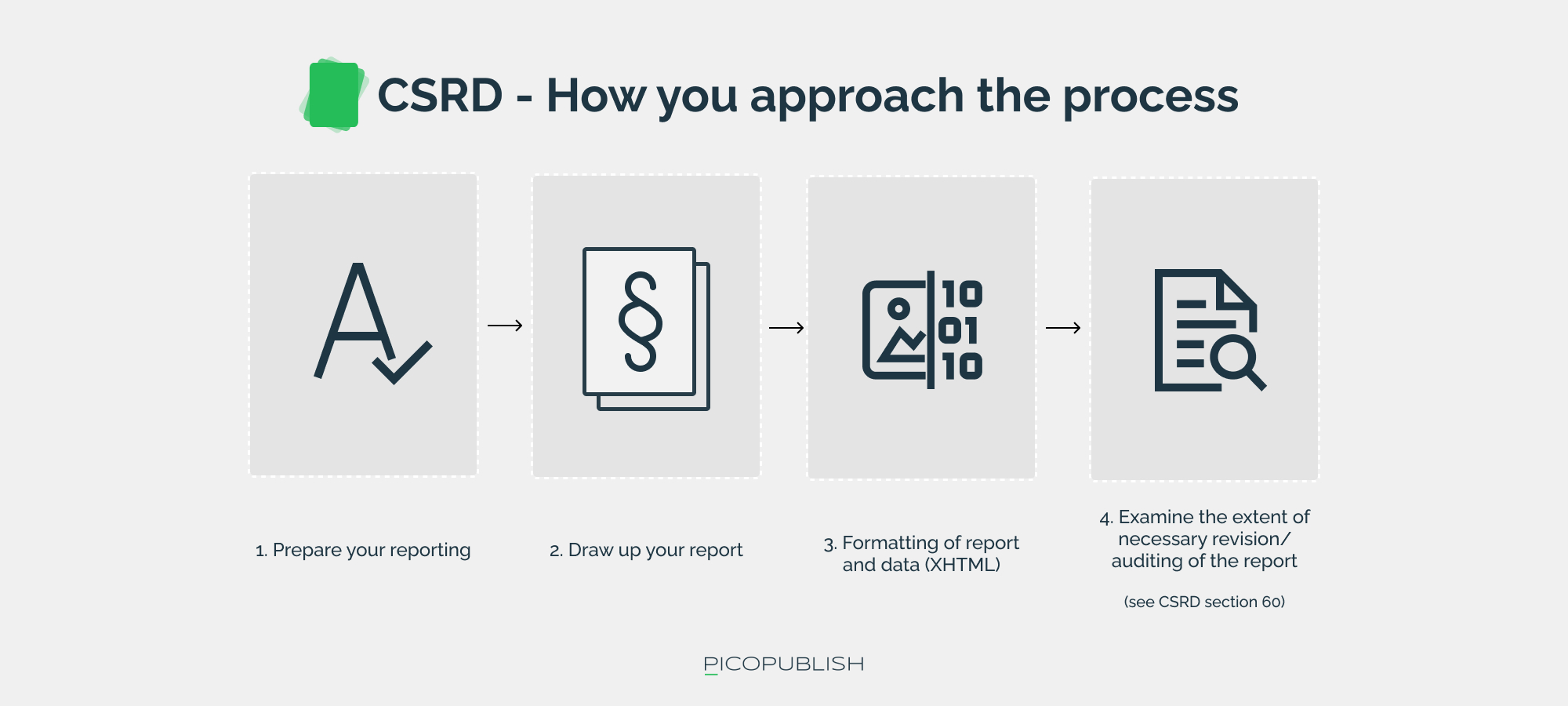

How do we approach our sustainability reporting?

Start by getting an overview of the process outlined by the CSRD Directive and the ESRS standard.

Broadly speaking, you must do the following:

- Set up a permanent working group responsible for reporting

- Conduct a double materiality analysis

- Analyze and map the company's impact on relevant ESG areas

- Prepare your sustainability report

The CSRD report aims to make companies aware of how they affect society and the environment around them, and how they intend to make a positive difference in these areas in the future.

What is the CSRD Directive and who is covered by it?

The CSRD directive from the EU requires companies with more than 500 employees to integrate sustainability reporting as part of their current management report.

This new form of reporting (often referred to as an "ESG report") represents an expansion of the financial statements that companies typically make today by including requirements for the addition of sustainability-related data.

According to the Danish bill on the implementation of the CSRD, large companies must include a separate section in their management report describing the company's sustainability impact and initiatives.

This section should contain information necessary to understand the company's sustainability impact and the impact sustainability issues have on the company's development, results, and situation. It is important that the company also describes the process it has used to identify the relevant information for the reporting.

This new form of reporting shifts focus from purely financial aspects to also include sustainability-related areas, and must follow the ESRS standard, which is divided into 14 categories with a total of 1144 measurement points. However, it is not necessary for companies to report on all points, but only those that are considered material based on the principle of "double materiality".

Double Materiality; Customizing the Reporting Scope

When companies - large and small - are about to start their sustainability reporting, they must first look at the ESRS standard to find answers to what data they should report.

To avoid all companies reporting on all 1144 measurement points in the standard, a principle of "double materiality" has been introduced.

This means that companies can choose to report only on matters that have a particularly relevant impact on people or the environment, or are of particular financial importance to the company itself. If a company opts out of a reporting area, they must account for the opt-ins and opt-outs.

As mentioned in the quote above, the company must provide information about "the process it has carried out to identify the information that has been included in the reporting" - and here the double materiality analysis is central.

CSRD's - Affects Both Large and Small Companies

Despite the fact that the directive initially only affects larger companies (500+ employees), we predict that smaller companies will also be affected.

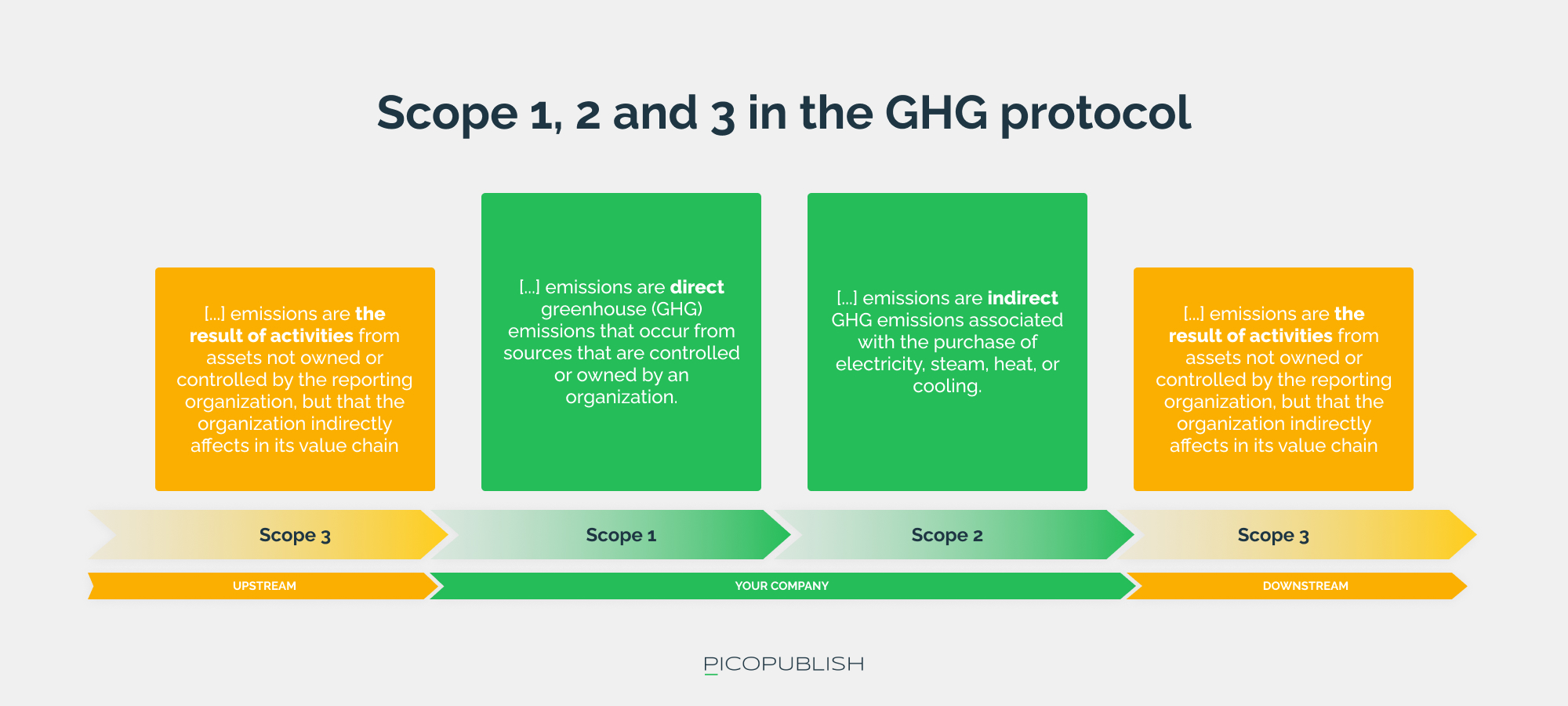

This is primarily because the companies that are directly affected by the new requirements must report on the total CO2E emissions in THEIR entire value chain (also called "scope 2" and "scope 3").

A consequence of this may be that a larger company chooses not to cooperate with a particular company if it cannot provide the necessary data. For smaller companies, the management and reporting of sustainability data therefore becomes a key issue when interacting with larger companies.

How does PIM support the work with CSRD?

The new requirements for sustainability reporting give affected companies an increased need to be able to work in a structured way with data. And therefore, there are many advantages associated with placing the PIM system as a central part of the collection, structuring and reporting of data that the new legislation requires.

How the PIM system supports the collection of sustainability data

For a typical manufacturing company, the so-called "Scope 3 requirements" will hit hard. The so-called Scope 3 requirements require companies to look at emissions (CO2E) in THEIR entire value chain.

In other words, companies that source materials, packaging, etc. from foreign players will have to keep accounts of, for example:

- Where do I buy my product?

- How far will my product be transported?

- How is my product shipped?

- ...And what does my Scope 3 accounting for CO2E emissions look like?

Companies will thus have to keep track of a significant amount of data that describes how they and their products affect the environment throughout the product's lifetime.

PIM systems are built with transparency in mind

Of course, the PIM system is not the only type of system that can support companies in their handling of the new data requirements.

On the other hand, the PIM system is built with openness in mind, and this makes developing integrations, automating enrichment, and exchanging data much easier than if you start expanding your ERP system.

If you want to make data collection more streamlined and easier for your trading partners, you could consider preparing a number of supplier data sheets that could be included in negotiations with your business partners.

We do NOT know that yet - consultation responses and criticism

In connection with the public consultation of the bill, various stakeholders have expressed their views on the upcoming legislation. The feedback that has been publicly presented points to a number of challenges and unresolved questions (https://hoeringsportalen.dk/Hearing/Details/67963).

Danish Auditors (FSR) - "A major transformation of reporting processes and systems"

In their consultation response, FSR points out that the upcoming requirements for sustainability reporting place great demands on companies. Specifically, they point to a number of challenges in the current interpretation of the bill:

- The bill is characterized by poor and imprecise wording, which makes it difficult to validate the content of the report

- It is to be expected that many companies, including the very large ones, may face difficulties in achieving a fully satisfactory level of sustainability reporting in the first years

- There is little or no guidance for understanding the requirements made

- It is expected that sustainability reporting will contain more estimates, uncertainties and assessments than the other general financial reporting normally contains

From the auditors, who are initially placed as a central part of the process of auditing to which sustainability reporting is also subjected, a picture is drawn of perhaps a little rushed and messy legislation.

For the same reason, FSR also states that they expect that in the first years of the implementation of the reporting, the requirements will be relaxed so that companies can find the right level and procedure.

The Danish Chamber of Commerce - "[...] the future ESRS standards will be extremely burdensome"

The Danish Chamber of Commerce represents a number of the companies that will initially be affected by the CSRD directive - including the ESRS standard. The Danish Chamber of Commerce has the following comments on the bill:

- The fact that the bill is not expected to be adopted until July 1, 2024, but works retroactively (i.e. as of January 1, 2024) is considered a breach of fundamental legal principles

- There is a lack of access to guidance for small and medium-sized enterprises - perhaps especially from the public sector

- The Danish Chamber of Commerce considers it crucial that the legislation in Denmark is proportional to the legislation in other countries. If the legislation in Denmark is too strict, Danish companies will have their competitiveness reduced

Remaining consultation responses

The remaining consultation responses can be read here: https://prodstoragehoeringspo.blob.core.windows.net/9301cfec-9110-44f5-8cde-4883dee48262/Samlet%20liste%20over%20h%C3%B8ringssvar%202.0.pdf